{kind=link}

Ever feel overwhelmed by steep interest rates and endless bills? It might sound a bit risky, but combining your debts could be the very first step toward making your monthly payments clearer and easier to manage. Imagine replacing a jumble of different due dates with just one simple bill, one that clearly shows where every dollar is going. In this post, we’ll dive into practical options you can use, like personal loans, balance transfer cards, or home equity lines of credit. Think of these tools as a way to ease your financial burden and set you up for a future where managing your money feels smooth and stress-free.

Key Debt Consolidation Options for Simplified Payments

Debt consolidation is a smart way to bring all your debts together into a single, easy-to-manage account. If you’re handling multiple credit cards, say one with an 18% APR, another at 22%, and a third at 24%, this strategy can simplify your life by combining them into one monthly payment. It’s like clearing out the clutter in your financial routine, making it easier to see where your money is heading.

Here are some common options:

- Personal loans: These offer a fixed interest rate and a steady, predictable monthly payment. You might face a small fee, usually between 1% and 5%, but the clear terms can really help you budget.

- Balance transfer credit cards: These cards often come with a low or even 0% introductory APR for a set time. Just keep in mind that they typically charge a fee of about 3% to 5% for the transfer.

- Home equity lines of credit (HELOCs): By tapping into your home’s equity, you might secure a lower variable rate and enjoy flexible borrowing and repayment options.

It’s important to remember that each method can carry extra costs, like origination or transfer fees, which can increase your overall repayment amount. So, before settling on an option, think about your credit situation, available assets, and how comfortable you are with the terms. This thoughtful approach can really help set you on a clearer path toward financial stability.

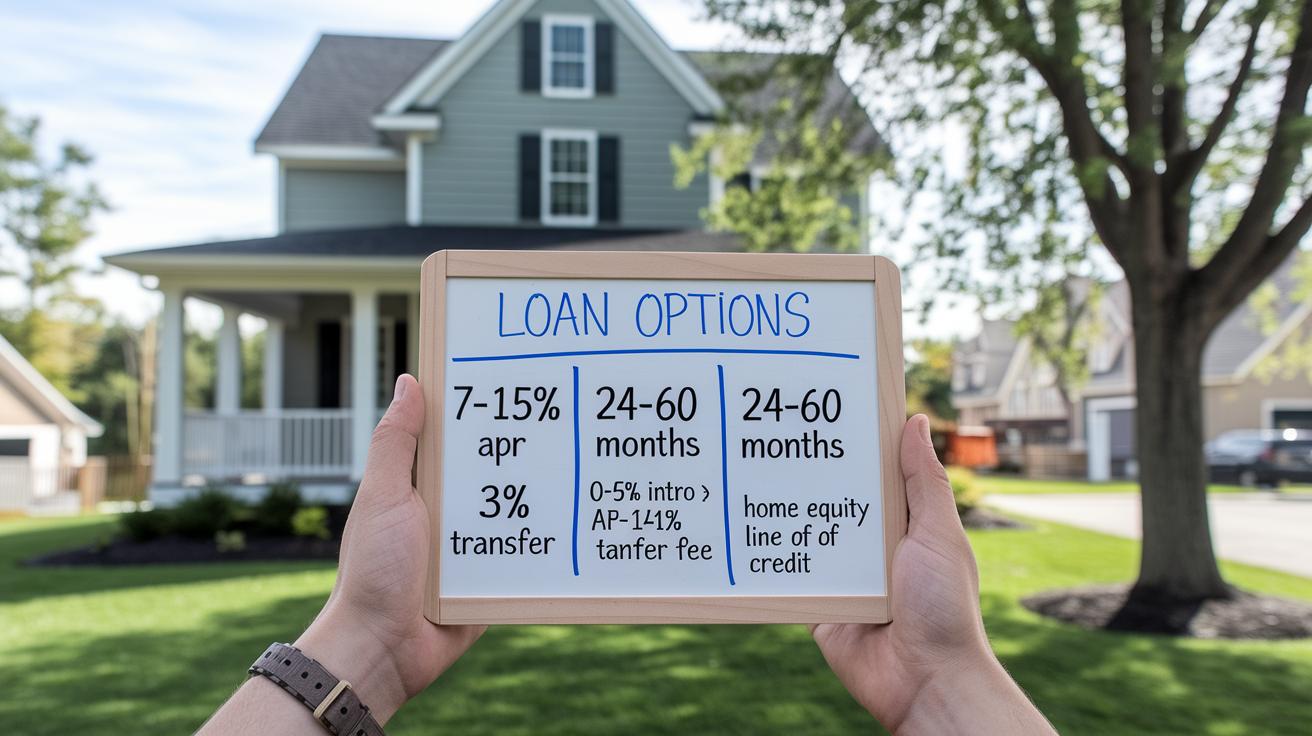

debt consolidation options: Smooth Steps to Relief

When you're looking at debt consolidation, it helps to break down your choices in a simple way. Personal loans come with a fixed interest rate, usually between 7% and 15%, and offer terms that last anywhere from 24 to 60 months. Balance transfer cards, on the other hand, bring an introductory APR of 0–5% for 12–18 months, though they typically charge about a 3% fee on the amount you transfer. Then there are HELOCs, they work a bit differently by providing a variable APR between 4% and 8%, and they use your home equity as collateral during an interest-only draw period. Each option has its own set of requirements: you might need a credit score of 620+ for personal loans, 700+ for balance transfers, and around 15–20% available home equity for HELOCs. This side-by-side view can really help you decide which method fits your financial situation best.

| Method | APR Range | Typical Fees | Eligibility |

|---|---|---|---|

| Personal Loans | 7–15% | Origination fees (1–5%) | Credit score 620+ |

| Balance Transfer Cards | 0–5% (intro APR) | Transfer fee ~3% | Credit score 700+ |

| HELOCs (debt restructuring) | 4–8% (variable) | May include annual or setup fees | 15–20% home equity available |

Choosing the right method comes down to factors like the interest rate, the term length, and whether the loan is secured. Personal loans shine with predictable, fixed repayments, which can give you peace of mind if you like certainty. With balance transfer cards, more of your payment initially helps chip away at the principal, though that benefit is only available during the promo period. Meanwhile, HELOCs offer flexibility with lower variable rates but require you to budget carefully since your home is on the line. Taking a close look at these differences, along with your credit score and what feels comfortable for you financially, can guide you toward the best debt consolidation strategy.

Debt Consolidation Eligibility and Rate Considerations

Getting approved for debt consolidation means you need to meet the lender's guidelines, which are usually based on a few key financial factors. Even a small change in your credit profile can affect your loan terms. For example, if your credit score drops by 20 points, you might see your APR go up by about 0.5 to 1%.

Here’s what lenders generally look for:

- Credit score: You’ll typically need a score between 620 and 650 for personal loans, 700 or higher for balance transfers, and 680 or more for HELOCs if you have enough home equity.

- Income-to-debt ratio: Most lenders expect this ratio to be 40% or less.

- Home equity: For a HELOC, having enough equity in your home is crucial.

- Documentation: Keeping your records timely and accurate can really help your case.

When it comes to rates, you have two main options. Fixed APR means your payments stay the same, providing consistency, while a variable APR might start off lower but can change if your credit profile shifts. It’s important to note that even small changes in your credit score can add up, impacting the overall cost of consolidating your debt over time.

Pros and Cons of Debt Consolidation Strategies

Let’s talk about debt consolidation strategies with a fresh perspective. Instead of repeating familiar points, we’re focusing on comparing your options through unique, practical insights. For example, a personal loan works like a pre-planned journey with fixed stops, while a balance transfer offers a short burst of no-interest relief. And then there’s the HELOC, which gives you flexible borrowing power but can shift unexpectedly, imagine your route suddenly changing if market rates climb.

Plan Comparison Tips

-

Look at the overall cost over the life of the plan.

Think of it like budgeting for a road trip: if your plan charges 4% interest over 5 years, calculate the total amount you’ll pay so nothing catches you off guard. -

Read the fee details to dodge hidden costs.

It’s like checking the fine print on your travel itinerary, unexpected processing fees can quickly turn a good plan into a costly detour. -

Make sure the repayment schedule fits your long-term goals.

Just as you’d align your monthly spending with your future plans, choose a repayment structure that suits your financial journey.

Tools and Next Steps for Debt Consolidation Success

When planning your debt consolidation, free online calculators can really make a difference. These handy digital tools help break down your monthly payments and even show you the total interest over time. This clear insight lets you see all your financial options without any guesswork.

You might try out a few different resources, such as:

- Loan calculators that help you estimate both your monthly payment and total interest, like using a debt payoff calculator.

- Rate comparison dashboards that pull offers from multiple lenders in just minutes.

- Lender review platforms that provide detailed reviews and terms so you can understand what each lender is offering.

Here’s a simple step-by-step approach:

- Start by gathering your current statements and downloading your credit report to ensure your numbers are spot-on.

- Use at least two different calculators to shop around and check for consistency.

- Compare pre-qualification offers across various digital platforms to see how rates and fees measure up.

- Only submit your consolidation application once you’ve confirmed which offer best fits your financial needs, so you know your plan really works for you.

Final Words

In the action, this article walked you through debt consolidation options by breaking down methods like personal loans, balance transfers, and HELOCs. It explained key fees, eligibility criteria, and step-by-step tools to simplify financial decisions.

We hope these insights help you evaluate your choices and boost your confidence in managing debt. With a clearer picture of your options, you’re set to make smarter budgeting and investing moves that lead to financial stability and growth.